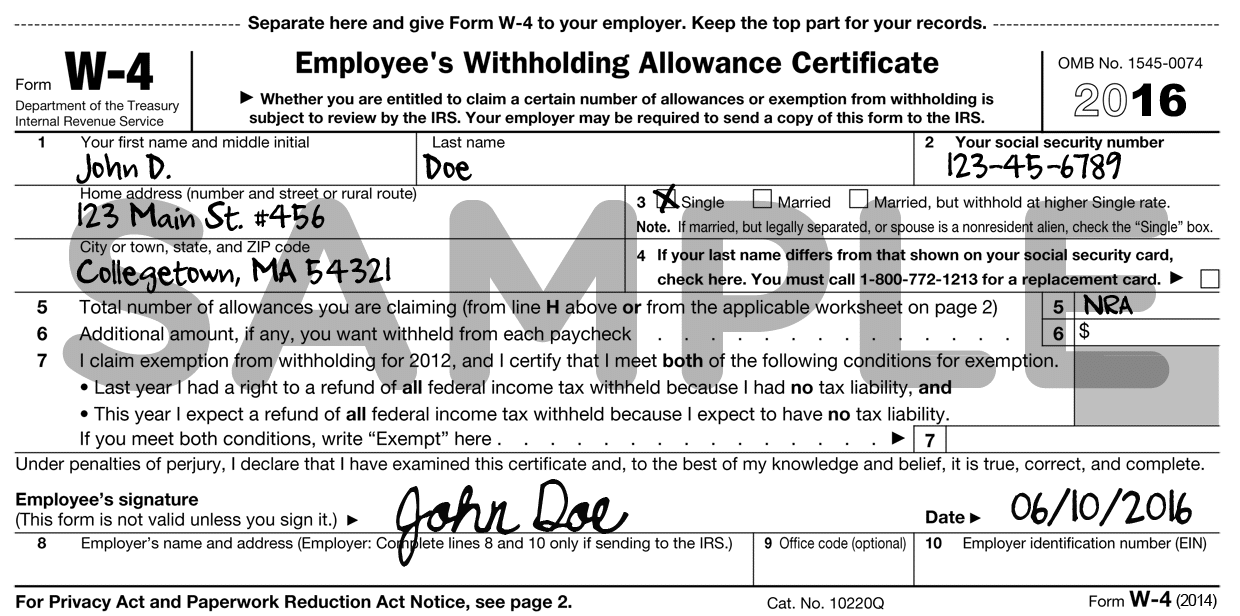

W-4 Form

All Exchange Visitors are required to complete a W-4 Employee Withholding Allowance Certificate when they begin working. This form determines how much federal, state, and local tax will be withheld from each paycheck.

Participant Responsibility

- The employer will provide the W-4 Form, and participants must complete and return it as soon as they start work.

- The W-4 form is used to calculate tax withholdings.

Correct Instructions for Nonresident Aliens

Many employers are not aware that J-1 Exchange Visitors are classified as “nonresident aliens” for tax purposes. This means that participants must follow the IRS Supplemental W-4 Instructions for Nonresident Aliens, not the general instructions printed on the form (which are for U.S. residents).

Key IRS Instructions for Participants

- Step 1(c): Check “Single or Married filing separately.”

- Step 4(c): Write “nonresident alien” (or “NRA”) in the space provided.

- Participants should not claim exemption from withholding in Step 4(c), even if they think they meet the exemption conditions listed on the form.

Role of Cooperators

- Remind participants to complete the W-4 right away when they begin work.

- Make sure they know to follow the nonresident alien instructions instead of the default W-4 guidance.

Filing a Tax Return

All J-1 Exchange Visitors are required to file a U.S. tax return after their program, even if they earned only a small amount of income. Cooperators should ensure participants understand the process and deadlines.

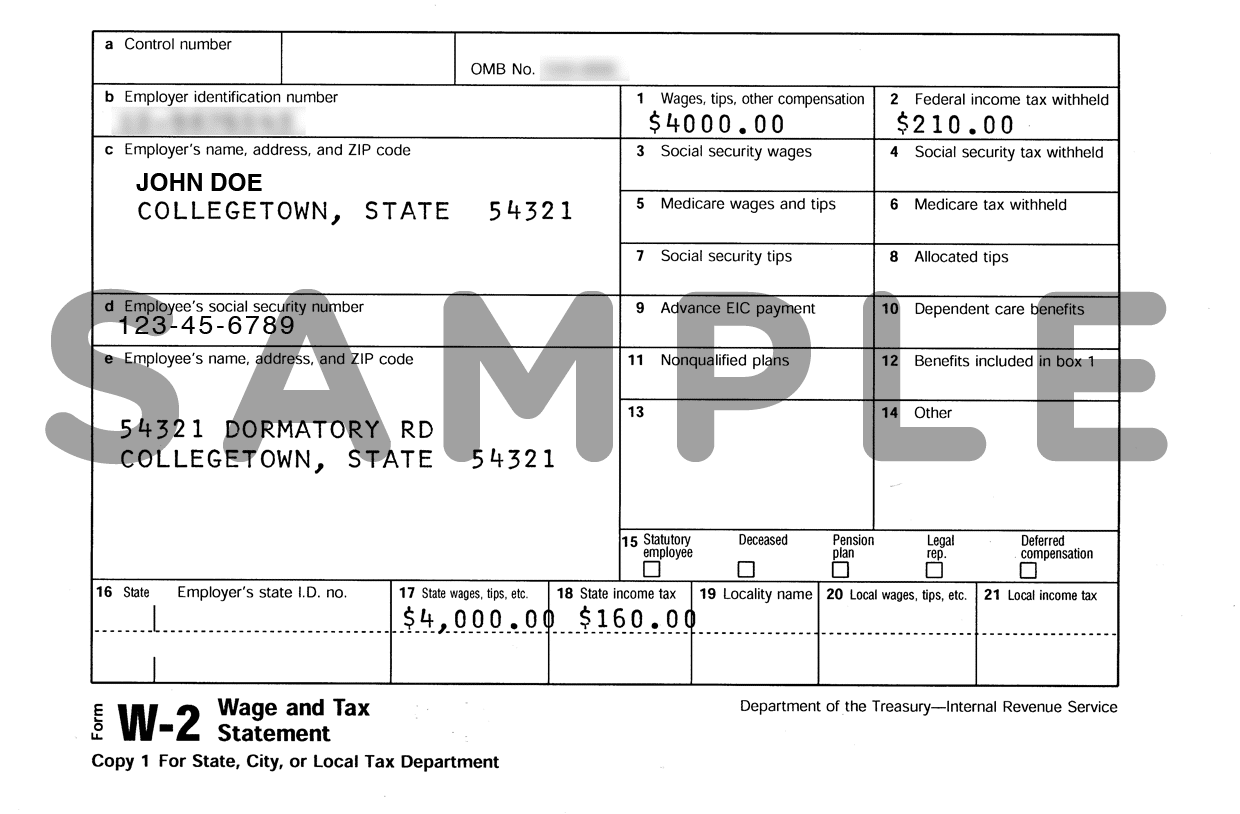

Step 1: Receive the W-2 Form

- Employers must send participants a W-2 Form by February 15th following the year of employment.

- The W-2 shows how much the participant earned and how much tax was withheld.

- Before participants leave camp, remind them to provide accurate mailing and email addresses so the W-2 can be delivered to them.

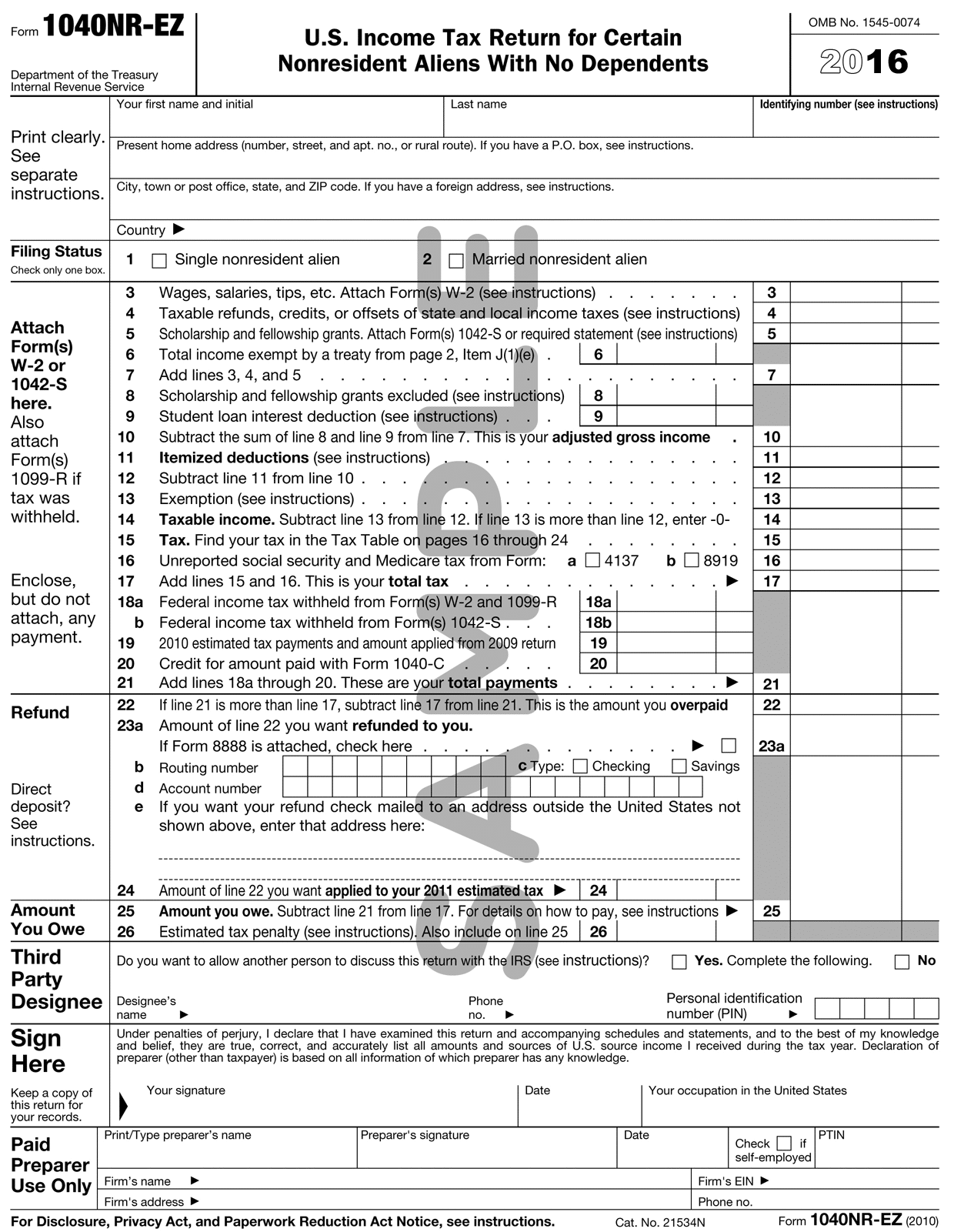

Step 2: Complete the 1040-NR Form

- Participants must file a 1040-NR (U.S. Nonresident Alien Income Tax Return)

. - They should carefully review the official IRS Instructions for Form 1040-NR before filling it out.

- Outcomes:

- If too much tax was withheld, participants will receive a refund.

- If not enough was withheld, participants must pay the balance owed.

- The filing deadline is April 15th of the year following their program.

- Many states also require participants to file a state tax return , in addition to the federal return. Each state has its own forms and requirements, usually available on the state’s Department of Revenue website.

Step 3: Submit Tax Forms

- Participants may mail their 1040-NR to the IRS address listed in the form instructions, or use an approved e-file service if available.

- Participants should always keep copies of all forms, receipts, and checks.

Mailing addresses:

- If payment is enclosed:

Internal Revenue Service

P.O. Box 1303 Charlotte, NC 28201-1303 USA - If no payment is enclosed:

Department of Treasury

Internal Revenue Service Austin, TX 73301-0215 USA

Refunds

- Refunds are usually issued as a paper check from the U.S. government. These may be difficult to cash in the participant’s home country.

- Direct deposit is possible only if the participant has a U.S. bank account at the time of filing. Participants should check with both their U.S. and home-country banks to explore options.

Role of Cooperators

- Remind participants about deadlines and required forms.

- Encourage them to check their mail and email regularly for their W-2.

- Help clarify that InterExchange staff are not tax advisors—if participants have detailed questions, they should seek assistance from a qualified tax professional or tax preparation service that works with nonresident aliens.